Central Bank Gold Buying – Latest Trends and Developments

Ronan Manly

Ronan Manly 0 Comments

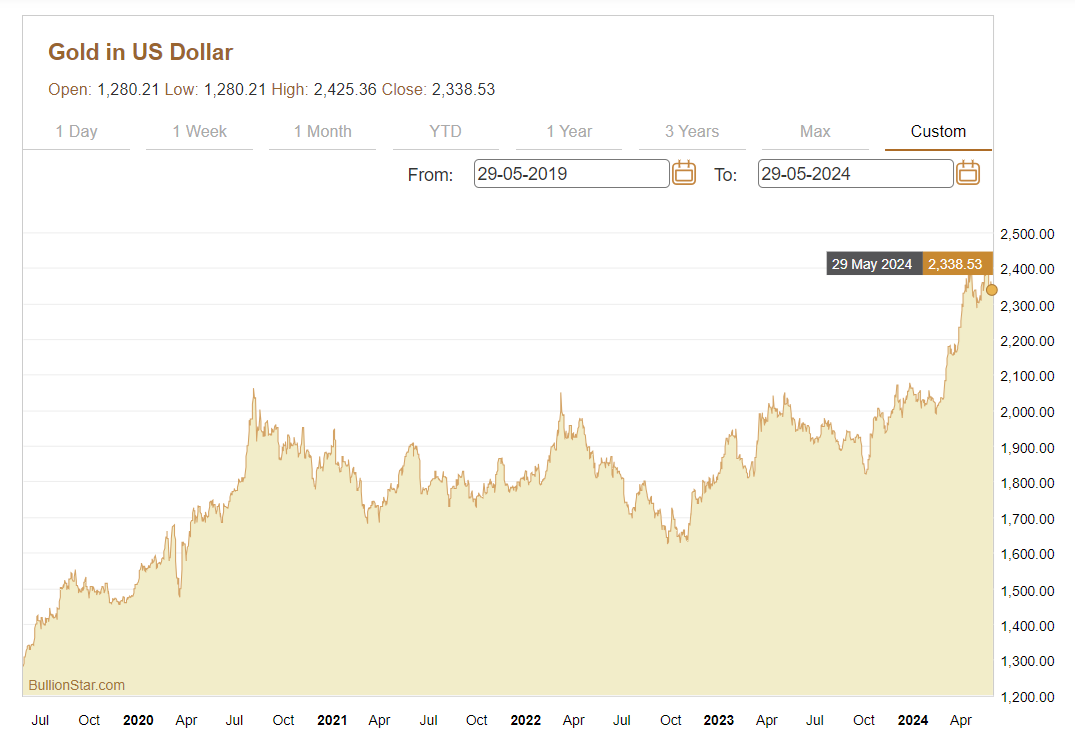

0 CommentsAs we approach mid-year 2024 in the environment of an all-time high US dollar gold price, its notable that central bank gold buying continues to be one of the main themes dominating gold market discussion.

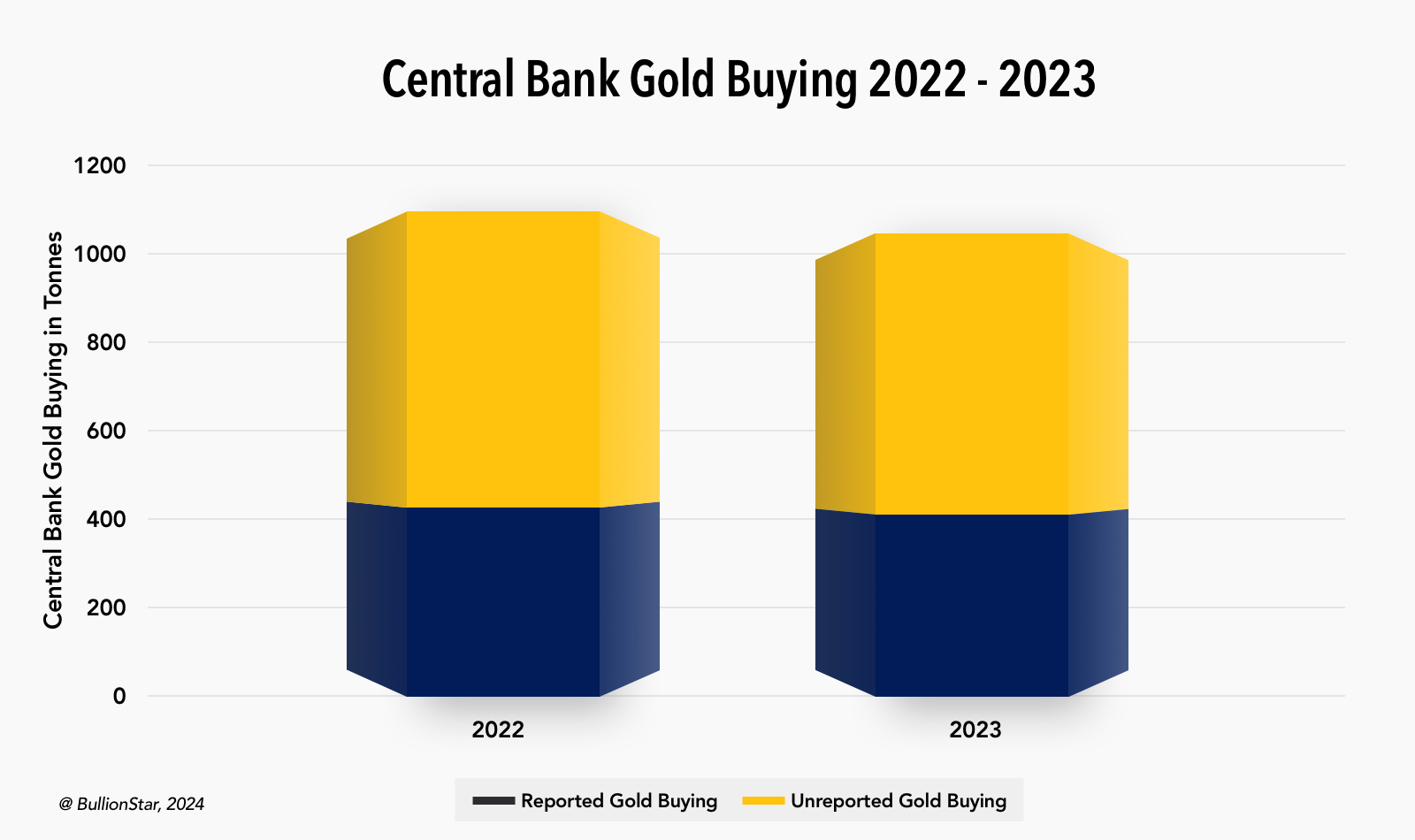

This is because following a record year in 2022, when according to the World Gold Council (WGC), central banks and official financial institutions across the world net purchased a massive 1082 tonnes of gold for their monetary gold reserves, the year 2023 was nearly as impressive, with central banks as a group buying a net 1037 tonnes of gold, just shy of the 2022 total.

Given that total gold mining production was 3625 tonnes in 2022, and 3644 tonnes in 2023, it can be seen that central banks are now responsible for buying the equivalent of between 28 – 30% of all newly mined gold.

Additionally, the recent buying means that, as of the end of 2023, central banks and official financial institutions held a combined 36,700 tonnes of gold, which was 17% of the world’s above ground gold stockpile of 212,580 tonnes as per WGC estimates.

Monetary gold buying activity has now continued into 2024, with central banks purchasing a net 290 tonnes of gold between January and March 2024, which again according to the WGC, is the strongest first quarter on record.

Unreported Buying

Before looking at which of the world’s central banks are driving this influential gold demand dynamic, its important to note that the majority of annual central bank gold demand estimates published by the World Gold Council comprise ‘unreported buying’, i.e. buying which has not been reported by any central bank but which has been ‘guestimated’ by the World Gold Council’s data collection agent, the London headquartered consultancy “Metals Focus”.

As the WGC Gold Demand Trends report said for 2022, central bank gold purchases were “a combination of reported purchases and a substantial estimate for unreported buying”. Since reported purchases in 2022 were only just 412 tonnes, this left 670 tonnes in the ‘unreported buying’ category.

A similar anomaly exists for 2023, a year in which the World Gold Council Gold Demand Trends (GDT) 2023 report didn’t even address the unreported buying guestimates, but glossed over them. In that year, reported central bank buying was 403 tonnes, which left a gap of a 634 tonnes in the unreported category.

While ‘reported purchases’ are based on actual central banks submitting gold purchase data to the International Monetary Fund’s (IMF) International Financial Statistics (IFS) database, ‘unreported buying’ is described by Metals Focus as “confidential information regarding unrecorded sales and purchases”. As such, this unreported buying cannot be verified and adds a lack of transparency to the data, since while Metals Focus claims it knows of these gold purchases, it won’t provide any details.

For a background on this inadequacy in the Metals Focus data, see the BullionStar article from November 2022 titled “Gold Establishment Supports Central Bank Secrecy”.

However, the magnitude of these unreported central bank gold purchases is to be believed, it seems that central banks have been spooked by increased sanctions risk and the unprecedented confiscation of Russia’s FX reserves by US and G7 sanctions, and are now increasingly buying the ultimate monetary asset which cannot be confiscated if stored in their home country national vaults – gold.

Gold & Gold Receivables – Possible Double Counting

Another caveat when looking at central bank gold buying data and central bank gold holdings in general is that there is no way to verify the accuracy of the data as a) central banks do not allow independent physical audits and b) the whole world of central bank gold lending is murky, where Gold & Gold Receivables are counted as one line item in central banks’ balance sheets, and where central banks and their bullion bank counterparts closely guard data on gold loans, swaps and leases. As such, there could be a lot of ‘double counting’ going on in the central bank gold world, where specific gold can be two or more places at the same time.

Which Central Banks are Active as Gold Buyers?

Now, having been made aware of these deficiencies in central bank gold buying and gold holdings data, let’s look at the central banks which have been reporting gold buying over 2023 and into 2024. You will see that the trend is mostly one of emerging markets, Eastern buyers, and BRICS central banks dominating gold purchases, while Western central banks (except those in Eastern Europe) remain for the most part on the side-lines.

People’s Bank of China

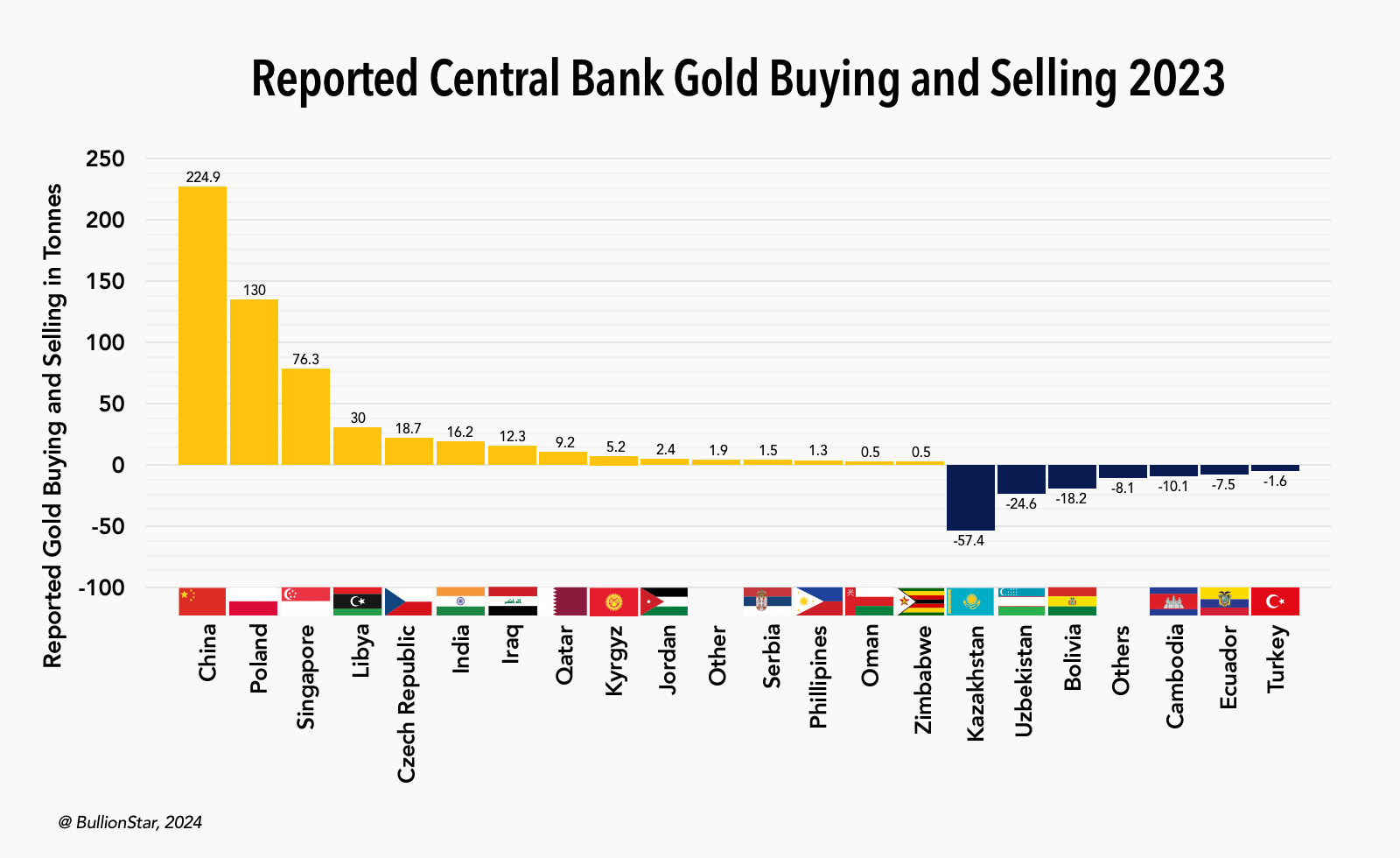

First up is the world’s foremost central bank gold buyer – China. Through its central bank the People’s Bank of China (PBoC), the Chinese state has publicly and steadily been accumulating monetary gold for 18 consecutive months now, each month announcing gold purchases via its State Administration of Foreign Exchange (SAFE).

Over that 18 month period, China has officially added a colossal 316 tonnes to its gold reserves, taking its official total from 1,948 tonnes of gold at the end of October 2022, to 2,264 tonnes as of the end of April 2024. These huge purchases allowed China to rank as the largest sovereign gold buyer in 2023 (with 225 tonnes).

The qualification ‘official’ is used here, for its very plausible that China has been accumulating far more gold than 316 tonnes over 18 months, but that it is only revealing a certain percentage of its purchases.

Importantly, the timing of China beginning to again reveal increases in its gold holding (which took place in December 2022 after a 3 year pause), coincided with the visit of China’s Xi Jinping to oil rich Saudi Arabia, a visit designed to strengthen Chinese – Arab nation cooperation and to signal increased independence from the West. For details see BullionStar article from January 2023 titled “Chinese Central Bank Accumulating Gold Again”.

The Polish Central Bank

The second largest central bank gold buyer in 2023 was by Poland’s central bank, the Narodowy Bank Polski (NBP) which accumulated a colossal 130 tonnes of gold last year over an 8 month period from April to November. This buying wouldn’t have come as a surprise to BullionStar readers, as we predicted as much in August 2023, saying that the NBP would purchase at least 100 tonnes of gold during 2023. See BullionStar article “Poland’s 50-50 gold buying : 50 tonnes bought over 3 months but another 50 tonnes to go” https://www.bullionstar.com/blogs/ronan-manly/polands-50-50-gold-buying-50-tonnes-bought-over-3-months-but-another-50-tonnes-to-go dated 2 August 2023

What was slightly surprising was that the NBP didn’t stop at 100 tonnes, and continued to buy gold during Q4 2023, ending the year with a grand purchase total of 130 tonnes.

Monetary Authority of Singapore (MAS)

The third largest sovereign gold buyer in 2023 was Singapore’s central bank, the Monetary Authority of Singapore (MAS) which accumulated a net 76.3 tonnes of gold between January and December last year, mostly front-loaded in Q1. Apart from its gold buying MAS also made headlines in 2023 when it for the first time ever allowed a camera crew to film inside its super-secret gold vault at an undisclosed location in Singapore. See BullionStar article from August 2023 titled “First Ever Filming of Singapore’s Super-Secret Gold Reserves”.

Interestingly, all three of China, Poland and Singapore have continued to make monetary gold purchases during 2024, proving that their gold buying was not just a 2023 calendar year phenomenon. The People’s Bank of China added another 29 tonnes of gold to its official reserves between January and April 2024. Poland’s central bank added another 4.7 tonnes of gold over March and April 2024 (is now the world’s 14th largest sovereign gold holder, with a claimed 363 tonnes of monetary gold)

And Singapore’s MAS announced gold purchases 6.6 tonnes over February and March 2024. Which was the first gold buying by MAS since September 2023.

Beyond these ‘Big 3’ of China, Poland and Singapore, many other central banks have been accumulating monetary gold in 2023 and going into 2024.

Czech Republic – The Czech National Bank (CNB)

In Eastern Europe, Poland’s neighbour the Czech Republic has been quietly and consistently multiplying its gold reserves since early 2023. This again will not come as a surprise to BullionStar readers, where in May 2022, we telegraphed the plans of the incoming Czech central bank governor Aleš Michl, to significantly augment the bank’s gold reserves.

“I will propose to have more gold, from 11 tonnes to 100 and more tonnes. Gradually, over several years. Gold is good for diversification, it has zero correlation with stocks." – Czech National Bank (CNB), Aleš Michl, May 2022

See BullionStar article “Czech Republic Joins Hungary & Poland in Gold Buying Binge”.

Soon after Michl’s interview, the Czech central bank gold buying programme began, and by December 2023 had bought 19.8 tonnes of gold, followed by another 6.4 tonnes in the first four months of 2024, for a total purchase of 26.2 tonnes. See IMF database here. So far, this Czech gold buying (which is now running for 13 consecutive months) has more than tripled the Czech National Bank’s (CNB) gold reserves from 11 tonnes to the current 37.2 tonnes.

Reserve Bank of India (RBI)

While India is famous for its retail gold demand and the huge scale of gold imports to satisfy that demand, for some reason the Indian central bank’s gold buying, although large and consistent, does not get as much media attention as say the gold buying states such as China and Russia. Despite this low-key media interest, the Reserve Bank of India (RBI), India’s central bank, has consistently added over 260 tonnes to its gold reserves since 2018, and now officially holds 822 tonnes of gold, which puts it in 9th position of the world’s largest sovereign gold holders.

After buying 42 tonnes of gold in 2020, 77 tonnes in 2021, 33 tonnes in 2022, but only 16 tonnes in 2023, this year looks more like the 2020-2022 era than 2023, for the RBI has already bought 18.5 tonnes of gold during Q1 2024, which is more than in all of 2023. Remembering that India, like China and Russia, is one of the five founding members of BRICS (and all three are now among the world’s top 10 central bank gold holders), this gold accumulation strategy by the RBI may be part of a longer-term coordinated geo-political strategy to prepare for de-dollarisation.

The Turkish Central Bank

The Turkish central bank is an unusual case when it comes to gold holdings as it sometimes sells gold to the domestic market to help meet local demand and then buys gold back again later. This happened in 2023 during a time when Turkish gold imports were banned but local demand was sky high. As such, Turkish central bank gold holdings first fell substantially by about 100 tonnes during H1 2023, and then rose by the same magnitude during H2 to leave the year unchanged. However, going into 2024, the Turkish central bank bought another 30 tonnes of gold during Q1, and now holds 570 tonnes.

North Africa and the Middle East

Across the Arab world, there is also a discernible trend of many central banks now raising their monetary gold reserves.

In June 2023, the Central Bank of Libya announced that it had purchased 30 tonnes of gold via a one off month-on-month increase. Iraq’s central bank claims to have added 34 tonnes of gold in 2022, another 12 tonnes in 2023, and another 3 tonnes so far in 2024, for a three year total of 49 tonnes.

Within the Gulf region, Qatar (a Gulf Cooperation Council (GC) member alongside with Saudi Arabia, the UAE, Oman, Bahrain and Kuwait) has been consistently buying gold since 2022, and has accumulated 46 tonnes of gold since early 2022, bringing its gold reserves to over 100 tonnes now. See for example BullionStar article “Qatar Ramps Up Gold Reserves as World Cup Approaches” from September 2022. Elsewhere in the GCC region, the Central Bank of Oman has been a buyer of 4.4 tonnes of gold so far in 2024. Oman had no monetary gold reserves before 2022, and now has 6.7 tonnes in total.

Russia

The last time that Russia announced significant monthly purchases of gold was over the March and April 2022 period, around the time of the Russian invasion of east Ukraine. Since then there have been few updates to Russia’s gold holdings, except sporadic announcements of monthly sales or purchases of about 100,000 ozs (3.1 tonnes) at various times, including for March and April 2024. But this doesn’t mean that Russia hasn’t been continuing to accumulate gold. Just that it hasn’t publicly revealed such purchases.

Central Asian Republics

Another group of central banks which regularly appear as actively transacting in gold are the central banks of Central Asian republics Kazakhstan, Kyrgyzstan, and Uzbekistan. This is because these banks frequently buy and sell gold from domestic production. The gold buying and selling by each of Kazakhstan, Kyrgyzstan, and Uzbekistan is more affected by domestic factors than anything else, and they could just as easily be buying as selling in any given month. These transactions skew the overall central bank gold buying data and can sometimes show up as net selling. For example, Uzbekistan net sold 38 tonnes of gold between the 15 month of January 2023 through to March 2024 but was a buyer for 6 of these months and a seller for the other 9 months. Kazakhstan net sold 57.5 tonnes of gold in 2023, but then was a net buyer of 16.5 tonnes of gold during Q1 2024.

There is also some central bank gold buying that is not recognised by the World Gold Council merely because it is not reported to the IMF. This includes gold buying by the central bank of Mongolia, which for example reported that it bought 14.2 tonnes of gold from local gold producers during the first ten months of 2023.

Central Bank Gold Buying Trends

Within reported central bank gold buying data, a number of trends are observable. Many of the major central bank buyers are from emerging markets in Asia and the Middle East, such as China, India, Turkey, Libya and Qatar. Some of the biggest gold buyers are members of BRICS, such as China and India.

The only OECD members countries publicly buying gold are Poland, the Czech Republic, and Turkey. As regards Poland and Czech, although they in the European Union (EU), they issue their own fiat currencies and are not in the Eurozone, so have more leeway in pursuing gold accumulation strategies compared to Eurozone members. Finally, its highly notable that the traditional Western central banks and G7 countries are not buying gold, and have not been buyers of gold for many years now.

According to the World Gold Council / Metals Focus, there is currently (since 2022) far more ‘unreported buying’ of gold by central banks than ‘reported buying’ that is tracked in the IMF IFS database.

Who could these unreported buyers be, if they do all in fact exist? They will most likely be central banks from Global South countries, a term which covers large swath of the developing world. They will probably be countries which are fearful of US / G7 sanctions and so want to rotate their monetary reserves out of G7 currencies and bonds and into counterparty risk free assets, gold being the logical choice.

‘Non reporting’ central banks may also include central banks from countries affiliated with organisations such as BRICS, the Shanghai Cooperation Organisation (SCO), and the Eurasian Economic Union (EAEU).

Central Banks’ Motivations for Buying Gold

A recent “Central Bank Gold Reserves Survey" published by the World Gold Council in 2023 backs up these observations about the enthusiasm of emerging markets central banks for gold.

Reflecting the responses of 59 of the world’s central banks, the survey captures the combined views of these banks about the role of gold in their respective monetary reserves (gold and foreign exchange being the two biggest components of monetary reserves)..

Survey respondents said that Interest rate levels, inflation concerns and geopolitical instability were the most important themes in their decisions to hold gold as a a reserve asset, and additionally “shifts in global economic power” was highlighted as an important theme by emerging market central banks. The survey also found that over 70% of central banks responding said that their gold reserves would increase over the next 12 months.

Compared to developed country central banks, a far higher percentage of emerging market central banks think that gold’s share of global reserves will be higher in 5 years time, and that the US dollar’s share of global reserves will be lower in 5 years time. Given that emerging market central banks have been the main central bank buyers of gold for the last decade, it’s not surprising that these banks are relatively optimistic about gold compared to the US dollar.

As to why central banks hold gold, the top six reasons stated by central bank respondents were – in order of importance – 1) “historical position” (77% of respondents saying that this factor it is highly relevant or somewhat relevant), followed by 2) “gold’s performance during times of crisis” (74%), 3) “gold is a long-term store of value / inflation hedge” (74%), 4) “gold is an effective portfolio diversifier” (70%), 5) “gold has no default risk” (68%), and 6) “gold serves as a geopolitical diversifier” (58%).

With regards to reasons 2-6 above for holding gold, a far higher percentage of emerging market central banks considered these reasons as relevant, again showing that emerging market central banks consider gold to be a highly strategic geopolitical asset and a financial insurance asset in the current environment of increased geopolitical risks amid the shift to a multipolar international monetary system at the expense of the US dollar.

Another interesting study, published in February 2024, is the World Bank’s “Gold Investing Handbook for Asset Managers”, which also recognises that “gold continues to play a critical role in the global financial system, serving as a hedge against inflation, a safe haven asset, and a reserve asset for central banks”

This study also highlights the trend we are seeing that “advanced economies have been diversifying away from gold reserves, while emerging markets have been steadily increasing their holdings”, which it says is being driven by emerging market central banks diversifying into gold due to “low interest rates on major reserves currencies”.

But importantly, the World Bank study also recognises that perceived geopolitical risk is driving emerging markets to increase their gold holdings, stating that:

“reserve managers in emerging markets tend to increase their gold holdings when there is a risk of financial sanctions. The largest increases in gold holdings by central banks often occur when the banks anticipate or face financial sanctions.”

Specifically, “both the volume and the value of gold reserves [of emerging market central banks] tend to rise in response to sanctions imposed by major economies such as the Euro Area, Japan, the United Kingdom, or the United States, in either the current or the immediately preceding years.”

Some examples of central banks increasing their gold reserves due to sanctions are the central banks of Russia, Belarus and Turkey. But it has been the sanctions against Russia which have really made emerging market central banks really sit up and take notice.

This has, says the World Bank authors, created a view that the world is transitioning from a Bretton Woods II era (which was backed by treasury bonds which have confiscation risks that can’t be hedged), to a Bretton Woods III era (to be backed by gold bullion and other commodities). This is the theory first put forward by Zoltan Pozsar.

Under this view, “Russian sanctions create incentives for central banks to abandon the dollar in favor of gold, and for governments to cash in their dollar reserves for stocks of other commodities [including gold]".

Conclusion

With annual central bank gold purchases of between 1000 – 1100 tonnes in each of 2022 and 2023, with “unreported” central bank gold buying in each of those years being in the range of 600 – 700 tonnes, this ongoing surge in central bank gold purchases (much of it clandestine) points to a significant shift in the international monetary landscape by the central banks of emerging markets, with a strategic move towards gold and away from the US dollar as a reserve asset.

There are many potential candidates for the central banks that are buying gold but not reporting it. While China does report some of its gold purchases, this is probably the tip of the iceberg and the Chinese state is most likely buying far more gold than it claims to be. Another candidate is Russia, which has been under intensifying Western sanctions where it would be foolish for the Bank of Russia and other Russian state entities to announce if they were buying gold.

Additional unreported gold buyers could be oil rich states such as Saudi Arabia and the United Arab Emirates (UAE) as part of a strategy to reduce dependence on the US dollar, and remember both of these nations are now members of BRICS.

Then there are other countries which are also facing western Sanctions and heightened geopolitical risks, such as Iran and North Korea, which too could be quietly accumulating gold and are among the ‘unreported buyers’ within the Metals Focus / World Gold Council numbers.

Despite the lack of transparency in unreported gold purchases, the substantial and sustained increase in central banks’ gold reserves highlights physical gold’s enduring role as a safe haven asset that has no counterparty risk. This gold buying dynamic is likely to continue, and indeed central banks themselves say it’s going to continue, as it reflects a broader move towards a multipolar financial system where gold plays a central role in preserving national wealth against geopolitical risks, while potentially being part of a new international trade settlement system.

Popular Blog Posts by Ronan Manly

How Many Silver Bars Are in the LBMA's London Vaults?

How Many Silver Bars Are in the LBMA's London Vaults?

ECB Gold Stored in 5 Locations, Won't Disclose Gold Bar List

ECB Gold Stored in 5 Locations, Won't Disclose Gold Bar List

German Government Escalates War On Gold

German Government Escalates War On Gold

Polish Central Bank Airlifts 8,000 Gold Bars From London

Polish Central Bank Airlifts 8,000 Gold Bars From London

Quantum Leap as ABN AMRO Questions Gold Price Discovery

Quantum Leap as ABN AMRO Questions Gold Price Discovery

How Militaries Use Gold Coins as Emergency Money

How Militaries Use Gold Coins as Emergency Money

Hungary Announces 10-Fold Jump in Gold Reserves

Hungary Announces 10-Fold Jump in Gold Reserves

Planned in Advance by Central Banks: a 2020 System Reset

Planned in Advance by Central Banks: a 2020 System Reset

China’s Golden Gateway: How the SGE’s Hong Kong Vault will shake up global gold markets

China’s Golden Gateway: How the SGE’s Hong Kong Vault will shake up global gold markets